By Joseph Gutierrez

Let’s take a quick look at whole life declared dividend rates in 2026. Remember, with whole life insurance, our Declared Dividend Rate is a calculated gross yield that is awarded to policyholders. Much like a dividend yielding stock like Proctor and Gamble, who will declare a dividend and payout to their shareholders; a participating whole life insurance company will do the same to their policyholders. If you are a policyholder or considering becoming one, we must understand that whole life carriers are essentially a cooperative. We share in the profit and expenses of the whole life insurance company, and we are awarded a dividend as co-owners.

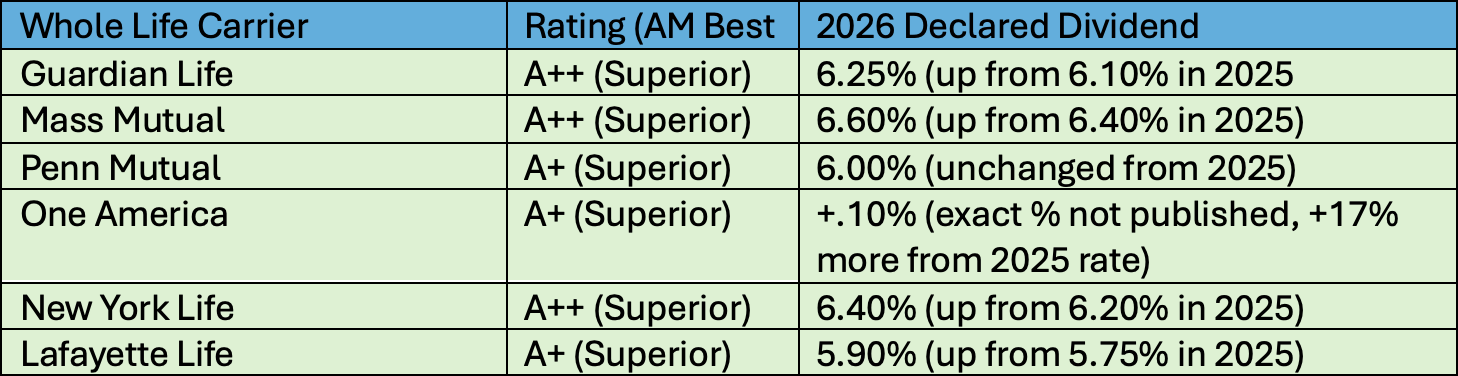

It’s also important to remember that while the guaranteed interest rate (usually between 2-4.5% depending on the paid up age and carrier), the dividend portion of our annual return is not guaranteed. The non-guaranteed dividend can be viewed as the excess from the insurance company’s General Account. The General Account consists of fixed income type assets like treasuries, corporate credit, and other bonds/low risk securities. The higher the interest rate environment, the better our return will be. While other people complain about high interest rates for this like home mortgages, whole life policy holders love higher interest rates because it means our returns continue to grow more every year. In the last few years, especially since 2022, we have seen interest rates climb and by extension we have seen whole life declared dividend rates (as well as annuity MYGA rates) increase. And 2026 is no different. The below table shows the current dividend declared rates for our favorite participating whole life insurance companies.

At first glance, the observer may think that because Mass Mutual has the highest declared dividend rate, then the cash value/death benefit will grow the best. Many of our clients are interested in building their tax free wealth with infinite banking so by this metric Mass Mutual should outperform the others, right? This is actually incorrect. Remember the declared Dividend Interest Rate is a gross yield that includes the guaranteed interest rate and the dividend (or excess).

The Dividend (yes I know its confusing, that’s just the terminology insurance carriers use), is a composite of the excess return from the General Account and discounted against the mortality costs and company expenses. Remember how we said we are policyholders that share in the profit and expenses of the company? This is where is shows up.

So to know which carrier will grow our cash value and overall policy the best, we need to shift our focus from Declared Dividend Rate, which only gives us part of the story and focus on the Internal Rate of Return on Cash Value/Death benefit. This will give us a better understanding of the growth rate of the policy and which carrier is best for us.

Now our IRR on Cash Value will be based on the policy design (Base amount, Term Rider amount, Paid Up Additions, age health rating, ect). Not to make it more complicating but the Internal Rate of Return is best discovered by running an illustration and tightening our variables so we can maximize our policy for our needs.

All that said, we have found the following to be true from our 3 favorite carriers:

Mass Mutual – A bit better for death benefit/estate planning purposes, high and good dividend, but not always the best IRR on Cash Value, great non direct recognition carrier

Guardian Life – Better flexibility, good IRR on Cash Value, Index Participation Feature may lead to even better Cash Value IRR, somewhat limited on total funding unless use different dividend options

Penn Mutual – Lower declared dividend but very efficient carrier, many times the highest IRR on cash value, good flexibility and great for taking income in retirement years with their Overloan Protection rider

Interested in building tax free wealth with whole life? Want the best return and most efficient policy design? Book a call with us today! No cost to consult, ever. Bring an illustration from another agent, we’ll be happy to take a look and see if we can beat it!