By Joseph Gutierrez

One of the great things about Indexed Universal Life (IUL) is its overall transparency, especially with its expense ledger. Unlike Whole Life, we are able to see a break down of our policy’s expenses and how it affects our policies growth. A simplistic way to view Indexed Universal Life is that it’s primarily a cash value accumulation product with some insurance slapped on top. In order for the IRS to grant policyholders the tax deferred accumulation and tax free access to our cash value; the insurance carriers have to follow basic IRS rules to maintain this status. This means that our policy must have some insurance based expenses to keep our policy in the tax-free insurance domain vs some taxable investment based account.

Understanding the basics on policy fees in IUL is critical towards making sure your policy performs and grows optimally year after year. So many times we see expensive policies that don’t do what the wanted client in the first place. Let’s first take a look at the various expense columns that divide up our policy fees and then we can take a brief look at how to minimize policy costs as a whole through good design principles.

Expense Types

Premium Load

Premium load is a fee on the premium that we are putting towards our policy, usually on the order of 5-10% of our annual premium. The premium load fee accounts for the insurance carrier in-house costs. Generally speaking, it revolves around overhead costs like admin fees, marketing and taxes. Yes, insurance carriers have to pay taxes too. Basically it covers internal costs associated with the insurance carrier running business.

Admin Fee

The admin fee is a fixed cost usually less than $100 a year. This fee accounts for policy maintenance like client servicing, web account maintenance and executing disbursement/policy loan features. Not a whole lot of nuts and bolts on this one, it’s allocated for account maintenance costs.

Per Unit Charge

Which is short for per $1000 dollar (unit) of permanent death benefit charge. This is a fee that sits on the ledger for usually up to 15 years. It is derived from the total permanent portion on the death benefit. Remember we mentioned that Indexed Universal Life is a cash value accumulation account with some insurance plopped on top? This cost relates to the permanent portion on the insurance that sits on top of the current cash value amount. Key word here is permanent portion but we’ll talk more on this later. This fee accounts primarily for the underwriting costs associated with getting the policy issued in the first place. The underwriters, the paramedical service, and the agent commission are tied to this charge. There is some overlap with the premium load fee with carrier overhead cost allocations but generally speaking it’s the cost to put policy in force.

Cost of Insurance

Pretty self explanatory; it’s the cost of insurance (COI)for that permanent portion of the contract. Sometimes the insurance carrier will refer to this as cost for net amount of risk but in practical terms it’s your permanent death benefit cost. To clarify: it’s the cost on the permanent portion of death benefit, not the total death benefit. So for example, if we have 500,000 of permanent life in our design IUL contract and our cash value is 300,000, then our total death benefit is $800,000. That said, our cost of insurance is based on that $500,000 of death benefit. This example assumes we are doing an increasing death benefit option, but for most of our clients it’s standard practice for cash value optimization. One thing to remember with Indexed Universal Life is that our COI do change as time goes on. Meaning, as we get older our COI cost will go up. Unlike Whole Life, the IUL cost of insurance tends to be lower in early years and then increases as time goes on.

Rider Charge

This stands for all optional riders that have an additional fee to attach to our policy. Riders like children’s term policies, waiver of premium riders and most importantly for our discussion, the supplemental term insurance rider. If we have some supplemental term attached to our policy then we will see the cost to carrying that rider in this column. Supplemental term is a very useful rider to make our policy profitable in the short and long run, which we’ll also see shortly.

Surrender Value

This is not a normally expensed charge in the traditional sense but we’ll make mention of it here. You’ll see this on policy ledgers for Indexed Universal Life and Fixed Indexed Annuities especially. There will be an account value/cash value side and then separate column for surrender value. The surrender value is the accessible cash value for disbursement/policy loans. In the first 10-15 years you’ll see a lower surrender value compared to the account value. That difference decreases over time until it’s $0 at the end of those 10 to 15 years, and the account value and surrender value equal each other. It’s similar to the concept of a vesting schedule like with a 401k. The employee needs to work a certain amount of years in order for the employee to get fully vested. That vesting amount ticks up every year until it gets to 100%. In a way, its a fairly similar concept to the surrender schedule of IUL.

Fundamentally, the surrender value is there for the scenario if a person was to walk away from their policy and cash it out completely. If the policy owner elects to cancel then they would receive the current surrender value amount. The insurance company does this to recuperate policy costs to cover their expense if the policy owner were to flat out cancel. Basically it makes the insurance company ‘whole’ on the transaction if the policy holder walks. If a policyholder doesn’t surrender their policy in those first 10-15 years, then they’ll never experience the any surrender charge. Remember Indexed Universal Life is meant to be life long assets that grow our tax free wealth into our retirement years. Now an additional important note: the Surrender Value is closely tied to policy design. If we design correctly, we can reduce the surrender value difference between our account value, thereby allowing us to have more access to our money in early years.

Policy Design

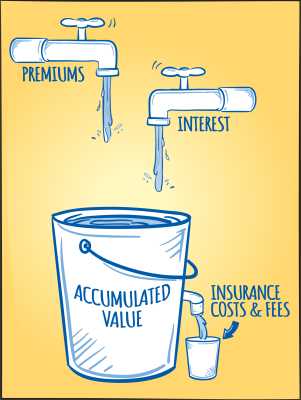

In insurance study manuals, Indexed Universal Life is often pictured as a large bucket (our IUL bucket) with water flowing in from the top and small hole on the bottom of the bucket. The metaphor is that water pouring into the top of it symbolizes our premium we are putting into the policy as well as the index crediting (usually averaging 6-8% per year). We can image it as pouring more water into our main bucket as we build up our policies total cash value(sometimes called accumulated value). On the bottom of our main IUL bucket is a small hole where water is coming out. The small hole symbolizes the expenses to keep the policy in force and compliant for the tax free advantages that we are looking for.

Now the trick in this metaphor is make sure our hole at the bottom of our IUL bucket as small as possible. It does us no good to put together a huge policy with excessive expenses because our bottom hole will be too large and thereby draining our policy before we can use it. Instead we want that metaphorical hole to be teeny-tiny.

How does this work in the real world? Well as we saw in our expense description, the majority of our expenses has to do with the permanent portion of our policy. Luckily, depending on the insurance carrier, we have access to term insurance rider (which is much less costly in the early years) that we can put in place of most of our insurance requirement. So for example instead of $500,000 of permanent life insurance in our policy; we can instead do a minimum of permanent insurance, example $100,000 permanent, and also $400,000 term insurance, for a total of $500,000.

As a side note, the IRS will allow us to ‘overfund’ a IULs cash value so long as we have enough death benefit attached. Good thing for us is that the term insurance portion counts towards that death benefit requirement. In our below example the Supplemental (ART) Term tends to be about 1/5 the cost of permanent for a health 45 year old male, per dollar of death benefit.

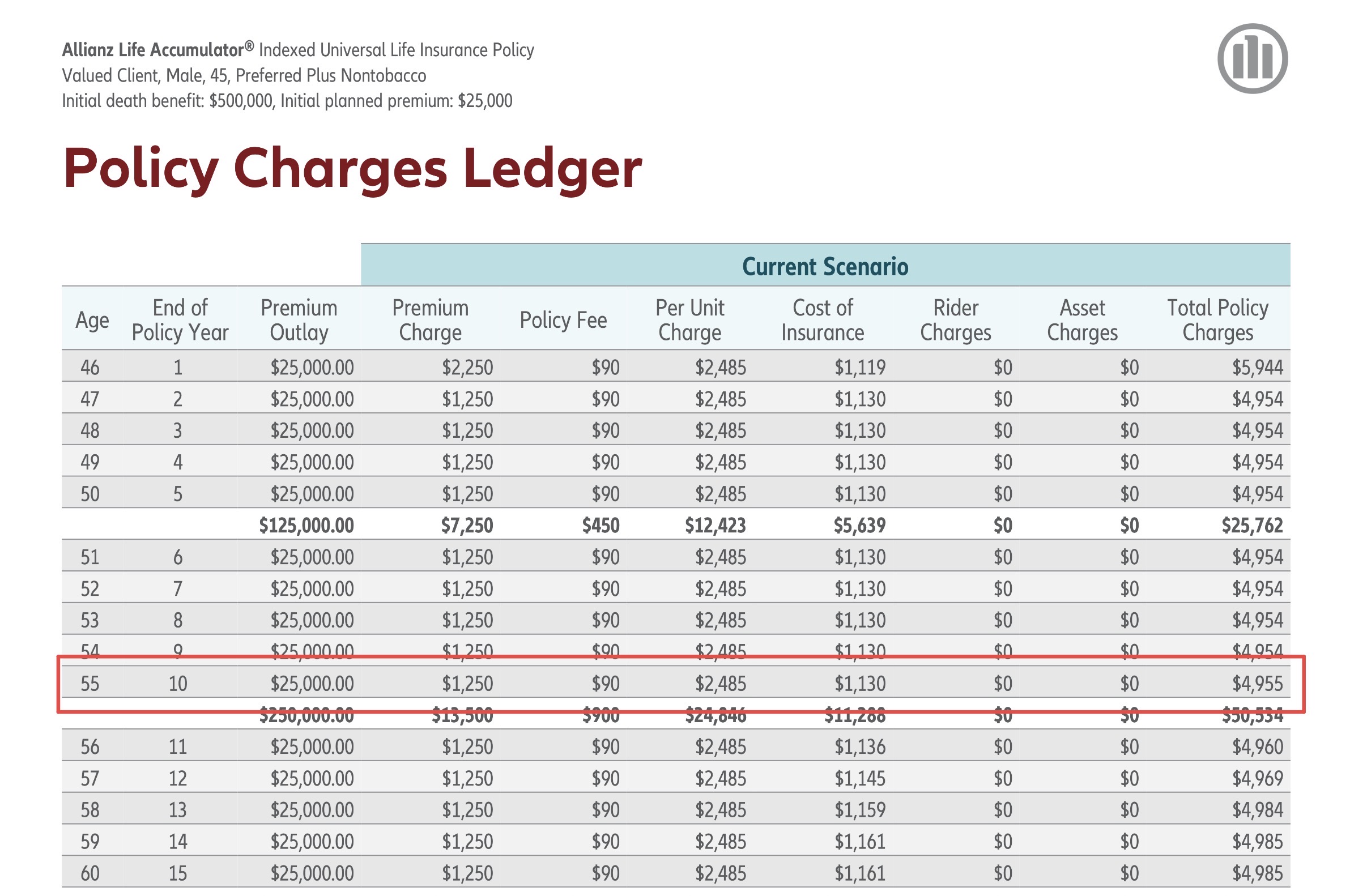

In doing so, our costs per year run from this:

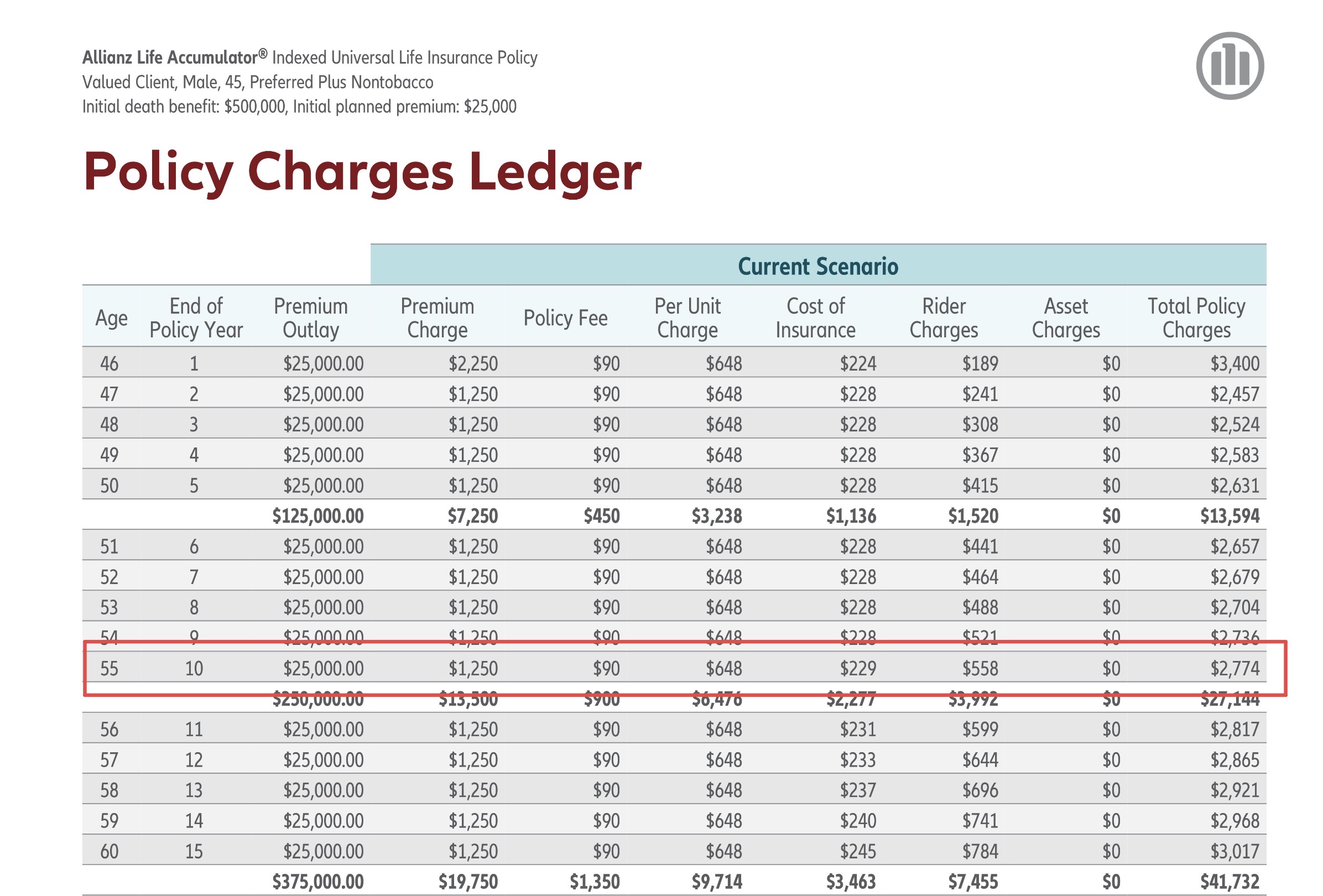

To something like this:

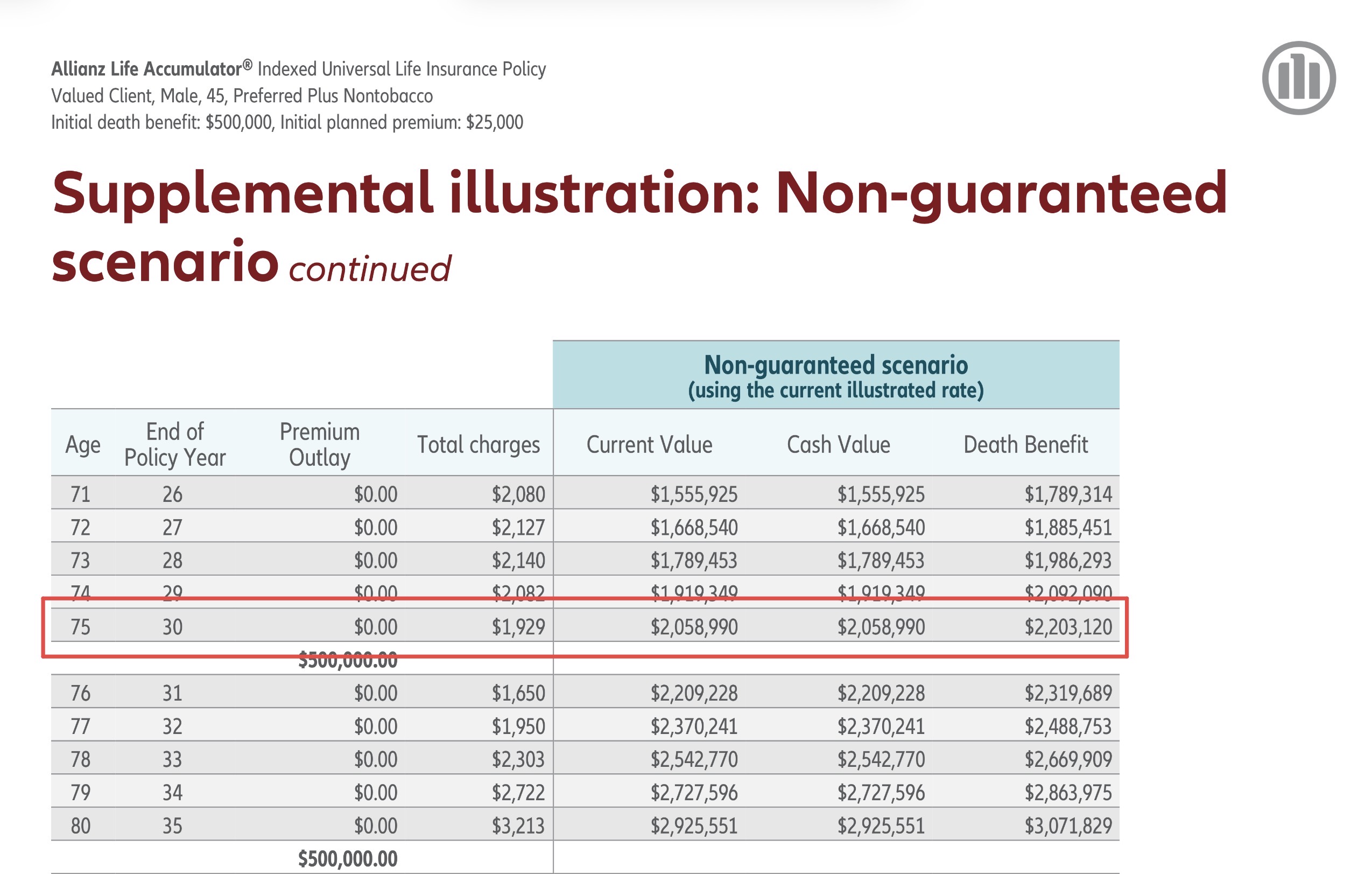

In our example here, the optimized policy with the term insurance rider lowered the expenses by almost half in the first 10 years! All those costs savings then get rerolled into our index crediting strategy, allowing much stronger cash values over time. Over a 30 year period, the cash value (and death benefit) can be on the order of 100s of thousands of dollars more in a more optimally designed policy. More cash value means more tax free wealth that we have built for ourselves. All with the same amount of input premium dollars.

And what about later in life when cost of insurance grow much more? Well when we are done funding our policy (say 65 years old), we can simply remove our term insurance rider/reduce the insurance to the minimum required. This essentially makes our bucket hole miniscule. And our cost against total cash value to something like .1% while we are in our retirement years. All the gain with next to no expense. Pretty cool huh?

For a lot of clients this may be the first time they’ve seen policies designed this way, where we infuse term insurance to lower our total expenses. Why don’t more agent incorporate this? Well remember that cost per unit column in our expense description and how much more it was that the blended permanent/term design? That number is the driving force to the agent’s commissions. So it goes to reason that agents best interests are to maximize the total permanent portion of the policy for their own pocket. But at the same time, this reduces the policyholder’s cash value. This leaves the average policyholder at odds with their own agent. Not good!

This is why working with the right agent/advisor is so important. It can affect your end cash value (as well as total death benefit) significantly. That’s why here at Covered and Compounding we make it a point to teach our clients first and place policies second. Our goal is to have happy clients that actively use their policy’s cash value in whatever needs, opportunities and/or grant themselves the tax free retirement that they deserve.

If you are interested in putting together your own custom policy and would like to see an illustration for your situation, book a free call with us! Have an illustration from another agent? Bring it to us and we’ll review it and see if we can do something better for you! Remember: the end policy design can mean the difference between 10s if not 100s of thousand of dollars in missed cash value. Don’t make that mistake!