By Joseph Gutierrez

When studying financial product and strategies, the inquisitive entrepreneur / investor may look at many different paths, different wealth generation vehicles. Stocks, bonds, real estate, farm land, starting/buying small business are all common vehicles to build personal wealth. That said, the savvy investor usually wants more. They dont just want AN ASSET, they want the BEST ASSET. They want stable growth. They want limited to no market downside exposure. Maybe something they can use as leverage. Tax free profits. But the number one thing that tops the list is passive income. Passive income seems to garner the imaginations of every investor. The problem though is that none of these common vehicles are truly passive. And if they have a passive element to them, they tend to have substantial market risk that defeats or ruins the whole model. I can buy bonds for fixed income but I have to pay tax on my gains and the bond market can fall apart (as we saw in 2022) and erode my principal. I can buy and hold stocks, but I don’t get much yield, and I’m exposed to market risk all the time. Not to mention, if I sell, I’ll have to pay capital gains tax. Real estate investing? As someone who invests and manages his own real estate portfolio, I can tell you that real estate is no where near to passive. No only that, but you are dependent on fickle and unpredictable input: the renter. Real estate can get expensive quick!

No, while all of these vehicles are viable great for gaining long term wealth, they aren’t particularly safe nor truly passive in the same sense.

We want an asset class that builds wealth for us in a passive manner and safe from market distress.

We want a passive asset that can be useful now, useful later in life AND if we can get it tax free then all the better. How can we accomplish all of these? Seems like an impossible task.

Well there is one asset that allows passive compound growth, safe principal protection, leverage abilities as well as tax differed growth / tax-free access aspects. It also happens to be the one asset class that everyone trips over. Permanent Life Insurance. Specifically Whole Life insurance.

Putting away the fear mongering from financial gurus and ignorant reddit users, lets peel back the curtain and see what is there. Whole Life insurance is a contract that provides a tax free death benefit to the owner’s beneficiary. It acts like a mini tax-free trust in a sense (although technically not a trust). Because the death benefit is tax free, if we honor basic IRS taxation rules, the cash value is also tax free and can be used throughout the life of the insured/owner.

This is where we need to focus on to understand the asset class potential. The Cash Value. Thats our growing, tax-protected liquidity that we can access (usually through policy loans) to deploy for our own benefit. If its a participating whole life carrier, then we have access to a guaranteed return and also an additional non-guaranteed dividend. This is our growth factor. Every year we get compounding effects from the guaranteed interest and non guaranteed dividend. And because they naturally grow the death benefit, they also growth the cash value proportionally.

The other misconception people have is that we have to fund a whole life policy through premiums every month/every year for the rest of our lives. This is blatantly untrue. Policies can be structured to fund for a short amount of time like 5, 10, 15 years or however long the owner of the policy wishes. Through concepts like Reduced Paid Up election; we can stop all future contributions to our policy and our cash value maintains its level and continues its growth even without further premium contributions. Yes, we can think of whole life insurance like planting and tree, nurturing it for the early part of its life and then letting nature take its course and grow for us. And just like planting an apple tree, we can come back a few years later and grab a few apples with little to no maintenance.

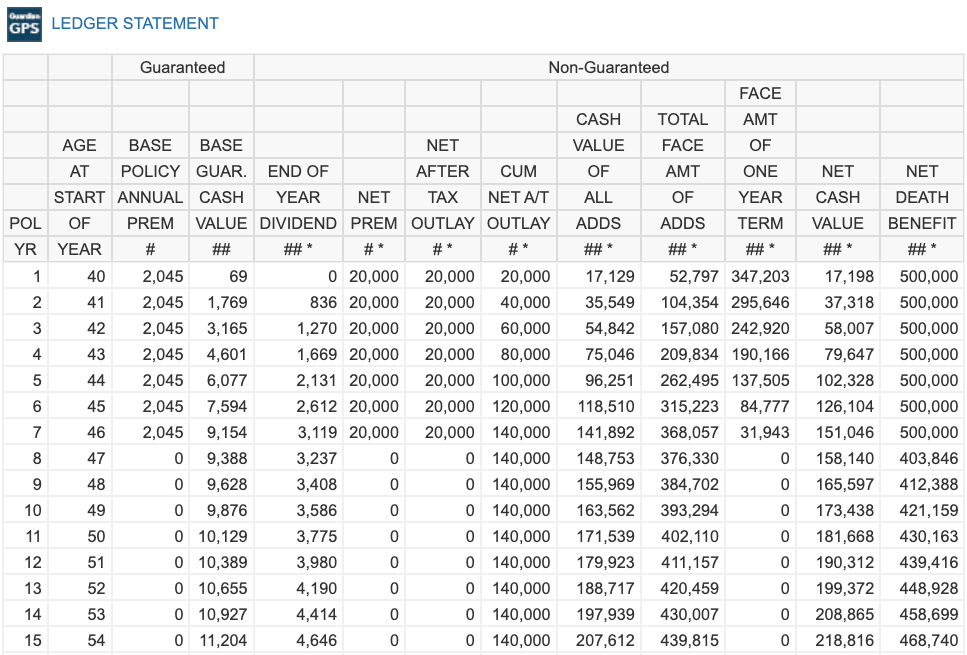

We’ll use the following example for context (see photo above). We have a 40 year old healthy male who funds its policy putting in $20,000 a year for 7 years. This policy was designed to maximize cash value and minimize unnecessary death benefit / other policy expenses. Just raw cash value growth with little else. We can see that $20,000 in the first year translates to $17,198 of cash value and $500,000 of death benefit. In our 8th year, our client doesn’t want to fund the policy anymore and elects for a reduced paid up. This is optional because the client can continue funding the minimum base premium of $2,045 to maintain the slightly higher death benefit if he wants. That said, for our clients goals, his main priority is to fund the policy and let it maintain and grow on its own and use it throughout life.

As we can see, our break even period where the cumulative premium = the net cash value takes place in the 5th year. This is where the policy turns us a profit in the sense of additional liquidity. This cash value can be seen as our own personal bank account. One that grows interest outside of the clutches of Uncle Sam and his tax schedule.

Now that we have the principal understood lets go over a simple example of use cases with real numbers.

Large Purchase

Lets say we are in the market for a new car. The car we want will run us $40,000. The traditional way of purchasing the car is with cash or most likely a car loan. In using a bank or the dealership, we may be paying 5 – 7% interest to purchase the car. But lets think about this little more. If we use an auto loan, we slowly pay off the car and gain title to the vehicle. But we trading something huge without realizing it. We trading that $40,000 of earning interest ability to and gave it away to the bank. We lost the ability to build on that $40,000. The $40,000 isn’t working for us any more. Its effectively gone.

Instead, what if we borrowed from our precaptialized life insurance policy and then pay ourselves back over time? What is the major difference?

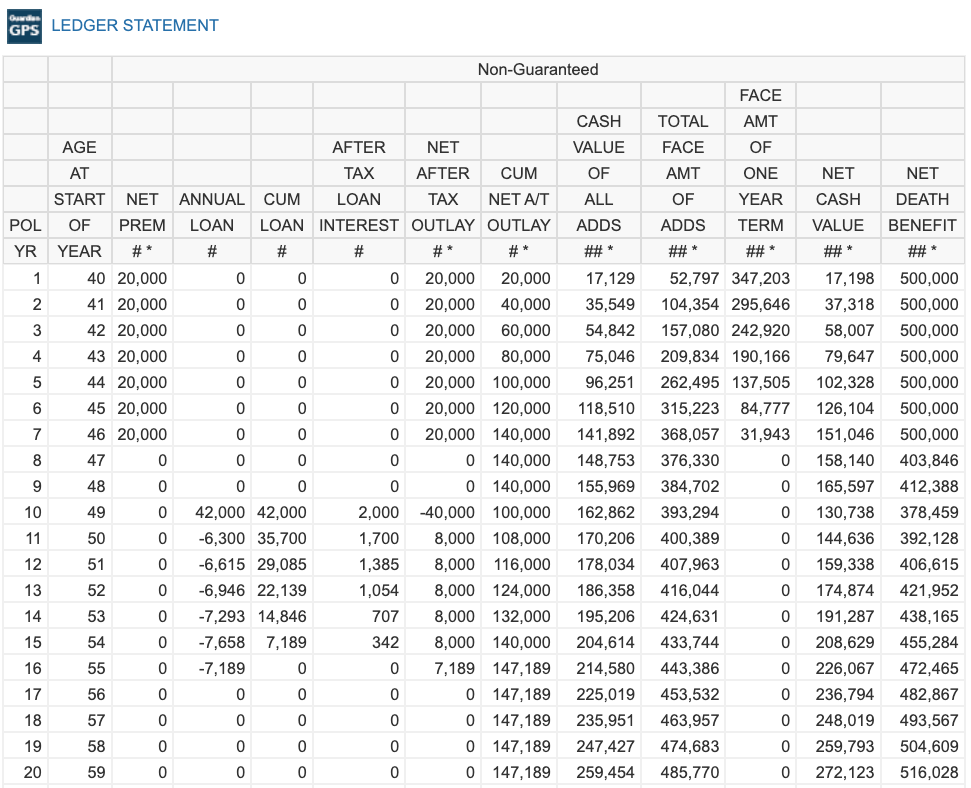

Instead we borrow the $40,000 from our policy against the cash value and use that to fund our car purchase. Then we can take however long we want to pay policy back. An important thing to note is that the insurance carrier doesn’t care if loans are outstanding or not because to the insurance company, they got to pay out that death benefit either way. So if there is a loan then they’ll just deduct the loaned amount from the death benefit (unless or until its paid off). This is true so long as we have a minimum required amount of cash value (5-10% range), to avoid any kind of lapse condition. In our example (see above), we didn’t even pay anything back into the policy for the first year. This is one of the added benefits of borrowing from our policy, we have loan repayment flexibility.

Beside the flexibility, the other obvious benefit is that our $40,000 was still working for us in the policy. Because its a policy loan, that $40,000 is technically from the coffers of the insurance company and $40,000 of cash value is pledged as collateral. And because our cash value is still safe in the policy; it is still growing with interest for us. Remember, these policies tend to have a + 4-5% tax deferred Internal Rate of Return over a 30 year period. The cash value prior to taking the loan came out to $165,597. We then borrow our $40,000 and pay our loan back comfortably over 7 years. At the end of those 7 years our cash value accrued to $226,067. This is what we mean by $40,000 is still working for us. Our example showed that we grew an additional +$60,000 in cash value during our payback period. Now of course we paid interest to the insurance carrier for the loan but we also grew on that full cash value amount in the meantime, the collateralized amount and non collateralized. Generally, policy loans are in the 4.5-5.5% fixed range giving us the added benefit of low loan interest costs.

To sum it up, with an auto loan, our $40,000 + the car loan interest disappears and all we are left with is the car. With borrowing from our cash value, we continued growing compound interest on our $40,000 (as well as the rest of our accumulated cash value), the interest was paid to the insurance carrier, but this loan helped us grow an additional $60,000 dollars in total cash value. And to be even clearer, of that $60,000 of total growth over the payback period, roughly $10,000-14,000 came from our $40,000 collateralized cash value. So in essence, we keep our $40,000 built an additional $10,000-$14,000 and got the car. Cool huh?

Investment

Now lets take this to the next level. What if instead of buying a liability or an expensive toy, what if we bought an asset? What if we bought an investment? Lets next model a real estate investment. Lets say we found a small mid 1980s 6 unit apartment complex in good condition. The downpayment plus closing costs plus a small amount of renovation will cost us $150,000. Now for the average investor $150,000 maybe a bit hard to come by, maybe its tied up in other assets or a 401k. Lucky for us we have this whole life policy we funded years ago accruing for us all this time.

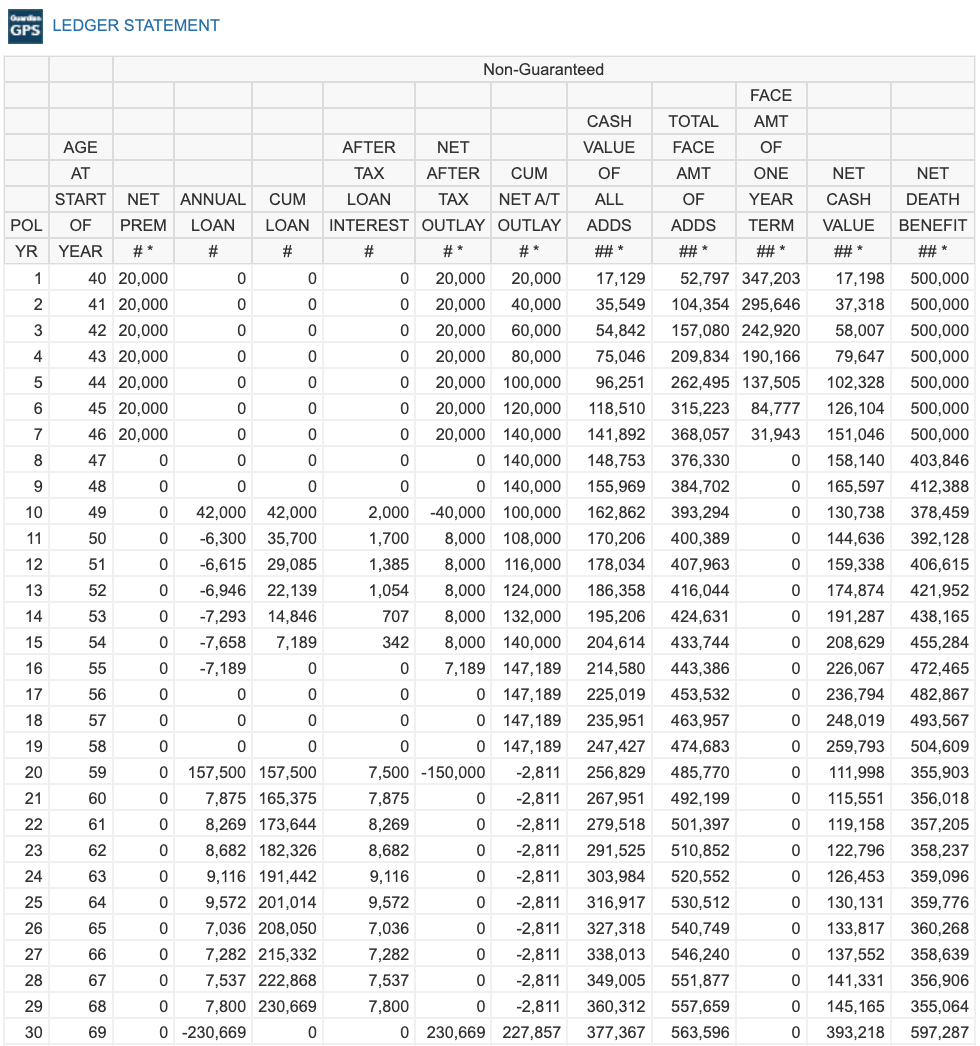

In our example above the owner is buying the property in his 20th policy year but we could have bought it much earlier. Generally speaking we can loan up to 90-95% of our cash value at any given time. As we can see from our example we reintroduced the same strategy but one major difference, we didn’t pay back the loan for a long time. No principal no interest for about 10 years. Again, unlike home mortgages or HELOCs where you have to make payments immediately; we dont have to pay back our whole life policy loan for years so long as we have adequate cash value. In this example our client purchases the property, stabilizes it, raises the rents, collects the rental income and holds it for 10 years. The owner can collect rent produced by the property as rental income and his policy is growing tax deferred cash value in the background. As we can see from our ledger (see above), our loan follows the same process. Our available cash value and total death benefit does decreases by the loan amount and our cumulative loan amount does grow over time, but the great thing is that our Total cash value column is still growing while we wait. Our policy has become an engine that can run itself, even with this $150,000 outstanding loan amount. This is one of the big ways that whole life insurance can build wealth over the long run. Passive growth and liquidity access.

And what about our clients exit on the investment? Well he can simply refinance and pay back his policy loan or just sell the property outright. In our example, by his 30th policy year he has paid back his loan with interest and his cash value has gone from $259,793 and accrued in the background to $393,218 after his loan pay back. Thats interest growth of $133,425 on his cash value! Almost equal to the initial policy loan! So our whole life policy paid for our investment, our investment paid us rent income and capital appreciation back when we refinance or sell, and we still accrued an additional $133,000 while we held our investment. We grew twice. We grew in our investment and we grew in our policy’s cash value.

I hope you can see why we see whole life insurance as the ultimate passive income and tax free wealth building tool. Many investors miss the generational wealth building ability of cash value life insurance but now you have the knowledge to use this asset to be the ultimate financial tool. Can you see why we call this the foundational asset? Uninterrupted, compound interest, that grows and we can access tax free.

Whats the caveat with all of this? Well, you do have to work with an insurance advisor that specializes in high early cash value whole life policies. Many insurance advisors don’t like putting these kind of policies together because it hurts their commissions. With us at Covered and Compounding, we just focus on giving our clients the very best the industry has to offer and be a knowledge resource so they can build their own family’s wealth. If you’d like help putting together your own maximized whole life policy for cash value accumulation click our link HERE and book a free online consultation. Have an illustration from another agent? Bring it to us and we’ll see if we can do something better! Thanks for reading and all the best.